How the banks wooed student customers: Cambridge, 1966

A collage of advertisements by English banks bidding for student customers in 1966 illustrates how banking culture has changed over six decades.

The advertisements appeared in the Varsity Handbook for 1966-7 which was published by the Cambridge student newspaper Varsity as a guide to university life, aimed particularly at newly arrived first-year undergraduates ("freshers").

Obviously, both the structure and the culture of the English (and British) banking sector have changed considerably over almost six decades. Eight banks were bidding for the custom of around three and a half thousand new students. Admissions to Cambridge were still dominated by independent schools, many of whose products would already have had bank accounts opened for them by their middle-class (and above) parents. I was a product of the State sector, but as I had worked for almost a year before coming up, two years earlier, I had an account with the National Provincial in my home suburb, with an arrangement to cash cheques at the Trinity Street branch. (I learn from the Internet that the first cash machines were introduced in 1967. Before that, if you wanted real money, you queued at your bank and cashed a cheque. Careful students would draw out as little as £5 at a time. It is no wonder there were 23 bank branches in Cambridge, a city of around 100,000 people.)

Obviously, the banks were competing for a relatively small pool of potential business. It may be that their advertisements in the Varsity Handbook were partly a commercial form of noblesse oblige, a public service gesture of support for a student activity in an academic community that allegedly produced future leaders. Nonetheless, the impression that the banks wished to project, that customers were actually valued as individuals, was primarily motivated by the assumption that people training for the professions would prove sources of a future comfortable flow of deposits. (I recall, but cannot trace, a bank advertisement from distant yesteryear in which an apparently impecunious young couple were urged to toast the husband's "half-million pound future": a salary of "a thousand a year", the classic middle-class threshold in the nineteen-sixties, would pump that sort of money through the vaults of a bank over a whole career.) Of course, even in the golden days of sixty years ago, banks were not always as nice as they pretended: the interfering and pompous Mr Mainwaring, the anti-hero of Dad's Army, was the branch manager of a Walmington-on-Sea bank as well as commanding officer of the town's Home Guard. (In one film version of the sitcom, the bank was Martins, presumably selected as it had long since disappeared.) I recall a friend at another university terminating a controversy with unsympathetic clerks by triumphantly writing a cheque to himself at a rival bank and closing the account. He has enjoyed a successful and remunerative career, and his persecutors must have cost their employer several millions in business.

The advertisements have a certain charm since they reflect the English banking sector on the eve of consolidation: by 1970, only four of them would survive as independent entities. In addition, as I note in a concluding section, both Cambridge and the student world in general were rapidly changing. The eight advertisements are arranged in four pairs, since they represent different approaches to attracting student customers.

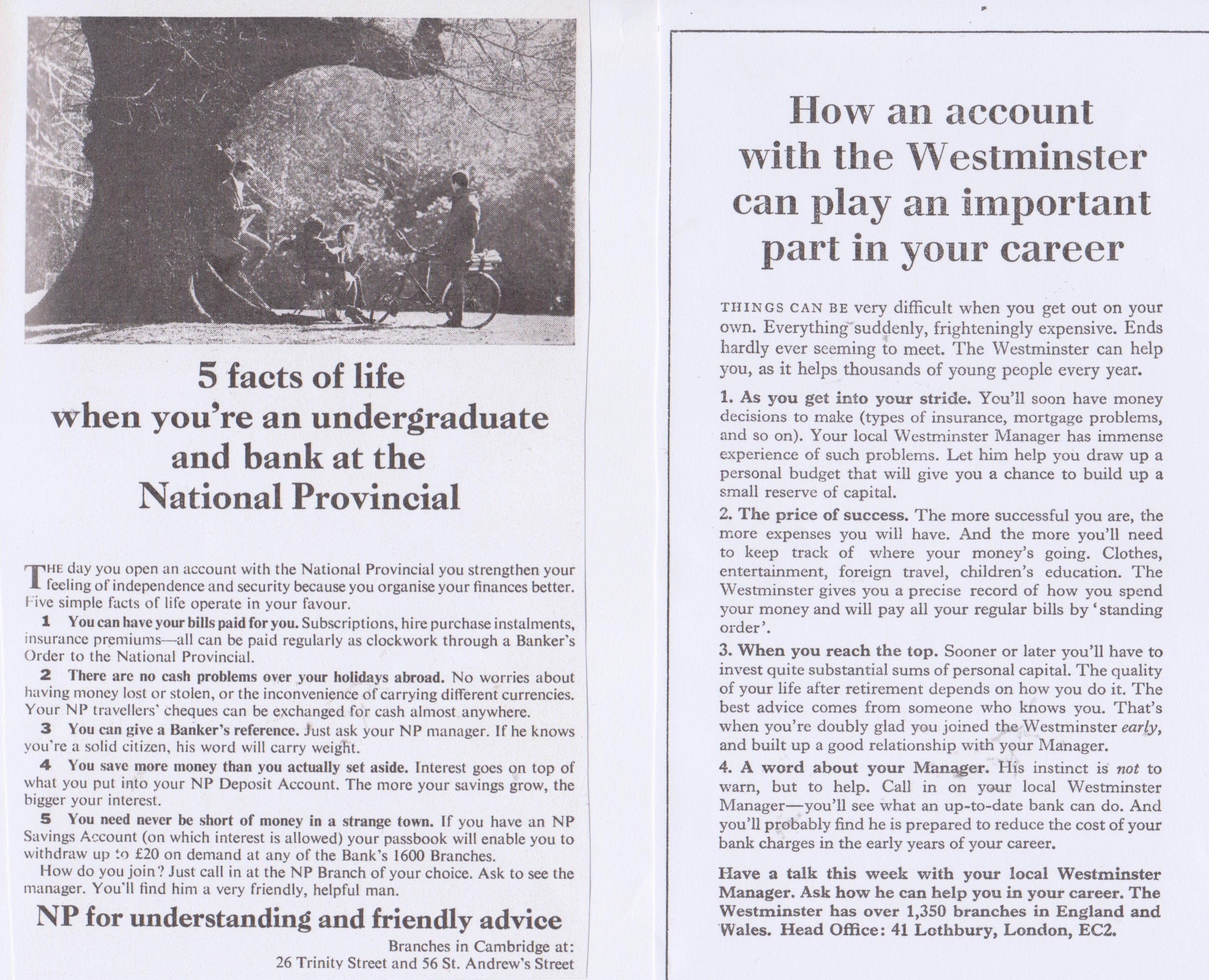

The National Provincial Bank and the Westminster Bank both adopted the Very Serious approach, cramming informative text into the small space. Curiously, the only aspect of student life that the National Provincial advertisement sought to address was foreign holidays, for which it could supply travellers' cheques. (This was hardly a unique banking service.) Two of its five numbered points assumed that students were able to save money. (Twenty-first century readers may be surprised to learn that there was an era when deposit accounts actually paid decent sums in interest. Of course, that was a long time ago.) Using the passbook from your National Provincial savings account, you could draw out up to £20 should if you find yourself in a "strange town". As a source of advice for undergraduates living on a grant in the very strange town called Cambridge, this was hardly very helpful.

The Westminster went several steps further, skipping the student experience altogether and rushing headlong into later life – mortgages, the expense of children's education (in private schools, it would seem) and even the need to plan for retirement. It may be doubted whether these themes struck many chords among teenagers seeking somewhere to deposit their first grant cheque. Both banks stressed the importance of establishing a relationship with the branch manager. At the National Provincial you would find "a very friendly, helpful man" – it was assumed that all career bank officials were male – who could provide you with a weighty bank reference, so long as he was assured that you were a "solid citizen", a coded reference for somebody who did not run up an overdraft. His counterpart at the Westminster was there "not to warn, but to help", although in practice an errant customer might find that the two functions tended to elide. However, it was hinted that Westminster managers had their favourites: it was important to sign up "early" to "build up a good relationship" which would help you to plan for your retirement. Sceptical students might perhaps have calculated that any bank official who became a father figure to them at the age of twenty would be long dead by the time they themselves were heading for the pipe-and-slippers phase of life. In any case, most students would leave Cambridge after three years. They might transfer their accounts to some other branch of the Westminster, but it is less likely that any relationship with staff would move too.

The Westminster advertisement dangled one carrot that the other banks did not offer. Get on well with your branch manager, and he would "probably" reduce your bank charges. In fact, in the mid-sixties, some Cambridge-based banks took the radical step of suspending charges on student accounts altogether. Armed with this information, I called to the National Provincial in my home suburb, and requested a reduction in the fees I paid. In that era, most male adults had served in the armed forces, either during the Second World War (and all honour to them) or through conscription, which continued until 1960. I suspect that rising to the rank of lance-corporal was one of the one of the ways in which aspiring bank officials demonstrated potential for reliability, although the achievement of promotion to non-commissioned rank was probably not the best training for the display of tact and charm. The assistant manager I encountered was openly sceptical of my report, and indeed closed the interview by telling me very firmly that he did not believe what I had told him. (In fairness, total suspension of bank charges was a breathtaking step, one which perhaps managers in the university towns were advised to keep under wraps.) I was mildly amused by the performance (and he did knock £1 off my charges, which represented an honourable draw), but I do have a strange dislike of being called a liar. Not long afterwards, impelled by a change in personal circumstances to review my financial arrangements, I bade farewell to the National Provincial.

No doubt all the bank advertisements were designed for general use, usually leaving space to include the address of local branches. These two made little attempt at individuality: the National Provincial crowded in its two Cambridge branches at the foot of the page. The Westminster's homily on Life omitted any allusion to locality. As it happened, these two banks – part of the traditional Big Five – merged in 1968 and were rebranded as the National Westminster – familiarly Nat West – in 1970.

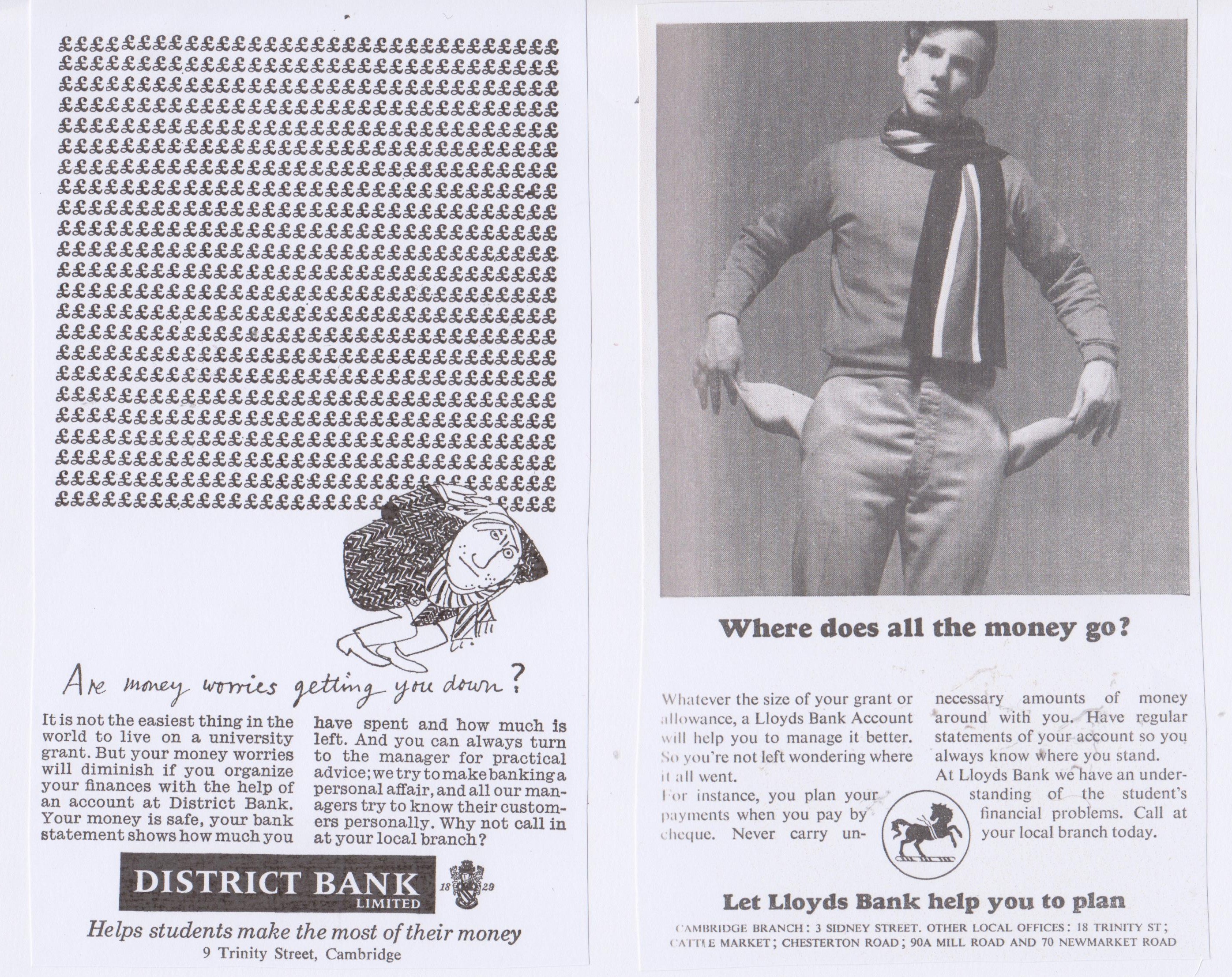

The District Bank and Lloyds concentrated on students' sense of insecurity about managing their own financial affairs for the first time. Both stressed the importance of bank statements as a means of managing payments and keeping in credit. Lloyds advised against carrying unnecessary amounts in cash. Like the National Provincial and the Westminster, the District Bank emphasised the role of its branch managers, who tried "to know their customers personally". This was perhaps a way of making the most of the possible objection that it was one of the smaller-scale operations in the financial universe. In fact, it had been acquired by the National Provincial in 1962, although it preserved its separate identity and Manchester headquarters until it was swallowed up in the NatWest label in 1970.

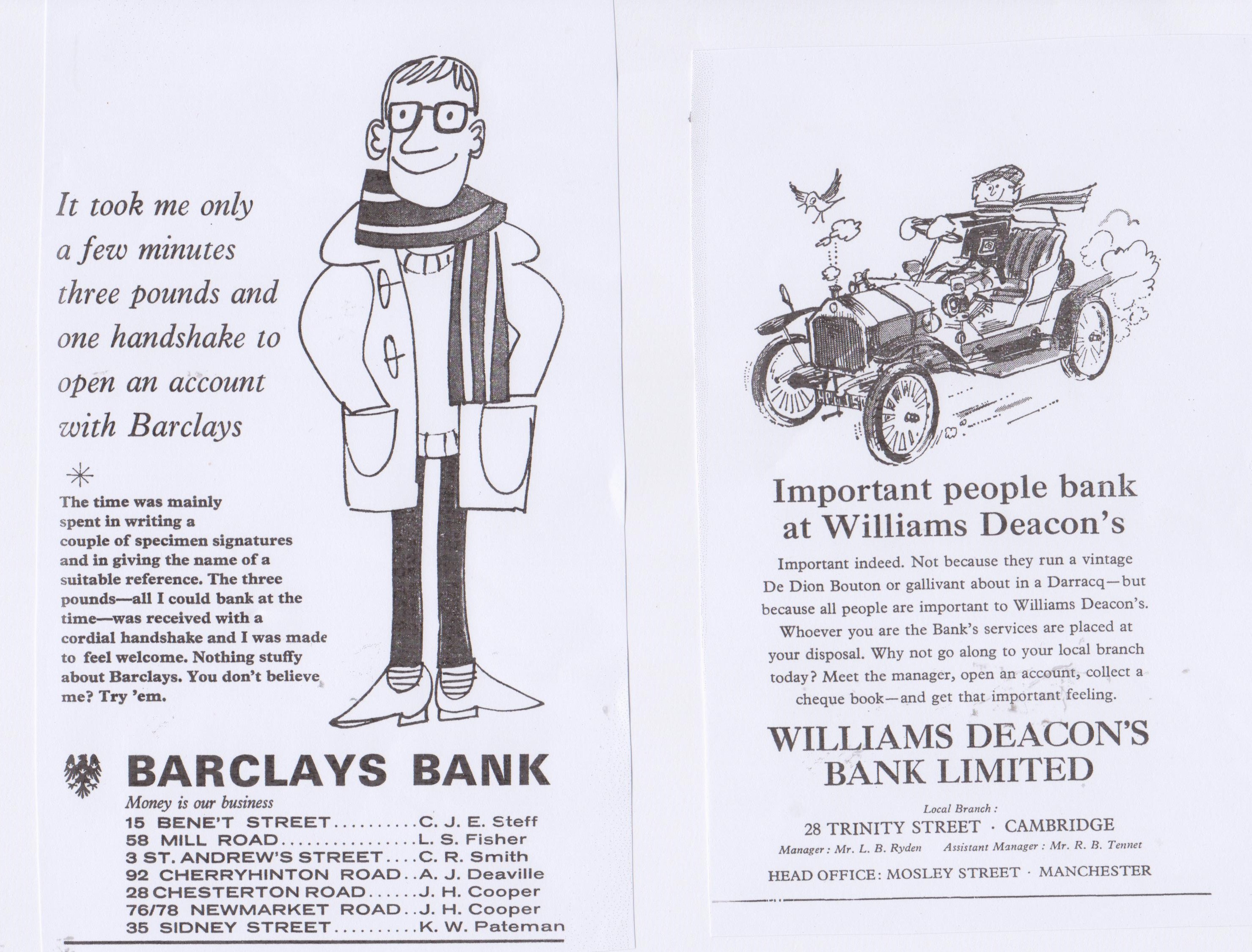

Barclays Bank and Williams Deacon's both tapped into the need to bolster adolescent self-respect. The duffel-coated youth who entrusted his finances to Barclays could only spare £3 to open an account (what had happened to his grant cheque?), but a "cordial handshake" made him feel welcome. "Nothing stuffy about Barclays." Barclays was the only bank advertising in the Varsity Handbook to specify that applicants had to supply a "suitable reference". In those distant days, banks were relaxed about proof of personal identity: possession of a grant cheque with your name on it was presumably thought to be conclusive. The passport was the only form of officially recognised photo-ID available in the nineteen-sixties: most Cambridge undergraduates had probably travelled abroad by the time they came into residence, either through school trips or family holidays, but passports were not generally called for as identifying documents. Williams Deacon's Bank went a step further in stressing its "people" credentials, shading into the eccentric approach of the final section. It was not necessary to drive a vintage car to be regarded as a special person: collecting your William's Deacon's chequebook would be enough to give you that "important feeling". Both banks listed their senior staff by name. Although it maintained an independent headquarters in Manchester – where it had opened a new building as recently as 1963 – Williams Deacon's had been owned by the Royal Bank of Scotland since 1930. In 1970 it became part of Williams & Glyn's Bank. Fifteen years later, it was merged into the Royal Bank of Scotland, and ultimately into the NatWest group.

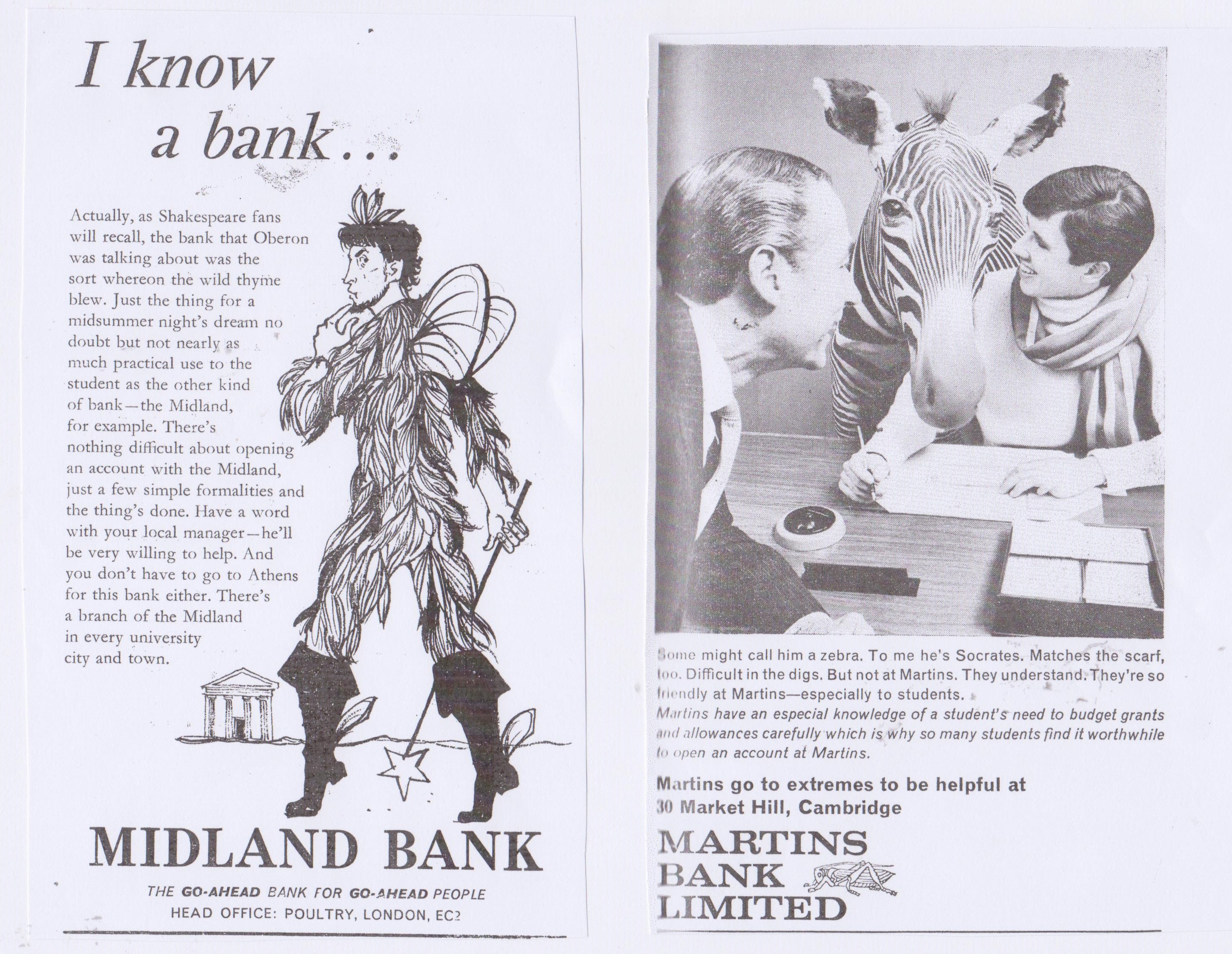

The last two advertisements were decidedly eccentric. The Midland Bank featured Oberon, the king of the fairies in Shakespeare's Midsummer Night's Dream, who knew "a bank where oxlips and the nodding violet grows", which was also the place where his queen, Titania, liked to sleep. For reasons that do not concern this study, Oberon decides to punish his wife by sprinkling snake oil over her slumbering eyes. The potion was intended to "make her full of hateful fantasies" which included falling in love with the first living creature she espies on awakening. This happens to be the cloddish peasant Bottom, who has unfortunately been turned into a donkey. My summary represents a considerable simplification of the plot, but enough has been revealed to suggest that the totality of Shakespeare's story hardly redounded to the credit of any financial institution seeking to project an image of probity. Although less specific than Barclays, the Midland also referred to "a few simple formalities" required to open an account. The advertisement was probably rather too clever for its own good. No attempt was made to localise it in relation to Cambridge – the Midland had branches everywhere, and intending customers were assumed to be smart enough to find the nearest. Perhaps students of English Literature were attracted by the gimmick, but they were hardly sufficiently numerous to make it worthwhile. (Nor were they likely to be the most employable potential high-income earners in the undergraduate market.) The Midland Bank passed unscathed through the upheavals of the late nineteen-sixties. However, in 1992 it was taken over by the Hongkong and Shanghai Banking Corporation. The Honkers and Shankers, as it was known in the solemn world of high finance, sought to relocate itself from Hong Kong, which was passing to Chinese control, and move its headquarters to London. In 1999, the Midland Bank was rebranded as HSBC.

If the Midland was puzzling, Martins Bank was downright zany. The intending customer's strange friendship with Socrates the Zebra proved that Martins "go to extremes to be helpful... They understand. They're so friendly." It was the only one of the eight advertisements to feature a photograph of a bank manager, viewed side-on but definitely a zebraphile. The copy was designed to give prominent space to the address, but the reference to "digs" in the text did not relate closely to Cambridge, where – by the nineteen-sixties – freshers generally spent their first year in college. The Wikipedia article on Martins Bank credits it with a number of "firsts", one of which was that it decided to "recognise and embrace the swinging 60's in its advertising". Unfortunately, and to my enduring regret, the mid-sixties in Cambridge barely managed the occasional wobble, and the approach may have bewildered rather than excited. (I should make it clear that, despite my surname, I had no connection with Martins Bank: had I possessed a dynastic voice in its operation, there would, of course, have been an apostrophe in the title.) It had its headquarters in Liverpool, and in 1969 was absorbed by Barclays. One pleasant continuing reminder of Martins Bank is an online archive. This includes a transcript of a visit to the Cambridge branch made by its in-house magazine in 1950, which described the staff in conventional terms, part team, part Victorian family. It may be read on https://www.martinsbank.co.uk/11-46-20%20Cambridge.htm.

In their drive to seem friendly and modern (the go-ahead bank for go-ahead people, as the Midland called itself), the banks chose not to dwell on the history of their commitment to Cambridge. Barclays might have claimed the crown, since it was the successor to Mortlock's, the town's first bank which had opened in 1780. Barclays absorbed its forerunner in 1896, but continued to operate its principal branch at 3 Bene't Street in premises built by the original founder, John Mortlock, sometime after 1783. The Westminster could trace its local roots to Humphrey's Bank, founded about 1825 and merged into the London and County Bank in 1846. The Westminster took it over in 1911, inheriting a huge and heavy Victorian building in Trumpington Street. This has been incorporated into the library of Corpus Christi College, which has charmingly blocked the front door with its impressive grasshopper clock. Fosters' Bank, operating by 1813, was absorbed into Lloyds in 1919. Lloyds Bank still operates from the Sidney Street building – designed by the quintessentially Victorian Waterhouse family architectural partnership – which overshadows Christ's College and seeks, through its knitting-pattern brickwork, to intimidate the cardboard transience of Petty Cury across the road. Stonework above a door still proclaims it to be Fosters' Bank, and there is no doubt about the plural apostrophe. The arrival of the other banks in Cambridge reflects the steady growth in student numbers: the National Provincial opened its first branch in 1909, the Midland in 1914, Martins in 1938 and the District Bank in the early nineteen-fifties.

It is striking to reflect that, in 2023, only two of the eight banks competing for undergraduate custom in 1966 survive under substantially the same name: Barclays and Lloyds (the latter having re-emerged in 2013 from a fourteen-year excursion as Lloyds TSB Bank). The Midland is now HSBC, while the National Provincial and the Westminster became the NatWest. After a rocky period in 1999-2000, NatWest was taken over by the Royal Bank of Scotland, but once again the strange logic of rebranding took a hand, and the NatWest name has emerged on top. It is strange to reflect that, with the exception of the Martins online archive, nothing survives of the remaining four institutions. In their day, they were major operations: the District Bank and Martins each had around 600 branches, Williams Deacon's over 250. Now they are forgotten.

Like the banking sector, Cambridge was in the process of change. In 1965-6, there were just short of ten thousand students, most of them undergraduates. If Cambridge was to be a world-leading research university, the balance had to shift. The first graduate colleges were taking shape in the mid-sixties, and this challenge forced the older institutions to take their own BAs more seriously. The gender balance was also absurd, with 8,800 men largely ignoring the marginal presence of one thousand women. (Homerton, then an independent teacher-training college, but very much part of the student community, added a further 500 to the female quota.) This, too, would change, especially after 1972 when the first three men's colleges became co-educational. By 2020-1, the academic community had grown to over 24,000 students, of whom 47 percent were postgraduates. Women made up 48 percent of the undergraduate population and 45 percent of the research students. The days had long since passed when all nine of the undergraduates pictured or cartooned in the Varsity Handbook bank advertisements were men.

Student culture was changing too. Five of the male figures depicted in the 1966 advertisements were wearing a striped college scarf. The college scarf did not disappear, but it soon ceased to be the defining symbol of a gilded and timeless undergraduate world that stretched backwards in decades. By 1968, the predominant tone was one of challenge to authority. Of course, it is possible to exaggerate the Cambridge manifestations of the student revolution, certainly in their frequency and probably in their intensity and depth. But the assumptions of 1966, which took for granted respectful probity and the pursuit of worthy careers, had become very dated. In retrospect, Cambridge in the mid-sixties was a startlingly innocent place. By the end of the decade, any student who claimed to be accompanied by a zebra was probably on drugs.

At national level, one casualty of this process of radical politicisation was Barclays Bank, which from 1970 became the target of an anti-apartheid campaign reacting to its dominance of the South African market. In basic business terms, Barclays could probably have ridden out the sixteen years of protests, but the company found it increasingly difficult to recruit the best graduates to renew its corporate leadership. In 1986, it agreed to divest itself of its South African subsidiaries. More recently, Barclays has been criticised for funding oil and gas projects, leading – as I write, in December 2023 – to calls for the University of Cambridge itself to transfer its business to a more climate-friendly institution. Once again, Barclays faces a student-led campaign to dissuade graduates from taking its jobs. Cambridge being Cambridge, there is – as ever – a twist in the story. It seems that the University never consciously decided to place its account with Barclays. In the nineteenth century, it presumably transacted its business through Mortlock's Bank, and Barclays simply took over when it swallowed Mortlock's back in 1896.

It hardly needs to be stated that the world has changed since 1966, and probably at a faster pace than in any other half-century in history. Naturally banking practice has evolved too. It is undoubtedly more convenient to be able to withdraw cash from a machine, at almost any bank or shopping mall, through a network that instantaneously creates a link across different institutions in disparate places. Even as a mildly technophobic senior citizen, I value the facility of being able to check payments and balances online, and occasionally I even manage to order a chequebook too (while this pen-and-ink vestige of the past may yet be tolerated). There is an understandable price to be paid for the shift to internet banking: Barclays, which operated seven branches across Cambridge in 1966, announced in 2023 that it was closing one of its last two outlets in the city. Of telephone banking, I do not trust myself to write, the more so as I am not resident in the United Kingdom and cannot know how far British banks have succeeded in overcoming its inherent disadvantages. All that is appropriate to point out here is that it would hardly have been possible in 1966 to have operated a customer-relations culture which mechanically assured frustrated account holders that their call was important but that the service was experiencing an unusually high level of people trying to get through. In 1966, there were 4.2 million residential telephone customers in Britain, plus another 2.2 million business connections. Spread across a United Kingdom population of 54.6 million, this equated to one private phone for every thirteen people, which suggested that even the middle-class people who held bank accounts were not all on the phone. If the telephone was used for banking purposes at all, it was probably to make an appointment to see a real person at the local branch. There are some compensations in having low levels of technology.

It is impossible to know how many eighteen-year-olds were swayed by these advertisements as they made their banking arrangements in October 1966. Those who survive will have turned 75 in 2023. If they still live in England and Wales, it is likely that many will have remained customers of the institution (or its successor) that they chose during their first Term at university, perhaps out of loyalty but maybe also through inertia. No doubt most members of that cohort have proved themselves to be, in the words of the National Provincial, solid citizens, who have generated much valuable business while causing their branch managers very few worries. Even if only a tiny handful were swayed in their choice of bank by the appeal to Midsummer Night's Dream or the prospect of holidaying abroad with a fistful of travellers' cheques, the cost of those advertisements placed in the Varsity Handbook fifty-seven years ago must have been recouped many times over.

For a list of material relating to the history of Cambridge on www.gedmartin.net, see:

https://www.gedmartin.net/martinalia-mainmenu-3/301-explorations-in-the-history-of-cambridge-by-ged-martin.